Last Thursday's market close was of interest to me. If we look at the SPX ( but any major index would do) we had an explosive lift off the earlier day falls that had made it look as though the bear army had already won the the battle of 1995 in SPX. But the following move up through 2010 was accompanied by a swift fall in the VIX too which has me thinking that this was the capitulation of the bears that I have been waiting for.

With this, my bull case has lost one of its main drivers. One of the other barometers of market direction has also swung - Fed, BoE and ECB expectations. These now appear firmly in the 'not for a long time' camp whereas a month ago they were in the field of 'tomorrow'. Meanwhile the macro position really hasn't seen any good news over the last month either to substantiate anything much more than this huge positional readjustment. With all this in mind I have trimmed my FTSE longs. I am sure there will be other opportunities to play coming along very soon but I'm not tempted to go actively short just yet. That will depend upon how Monday trades and though my suspicion is for a roll over, my key indictor will be copper.

Finally I'd like to introduce you to a very powerful chart formation - The 'Crouching Polemic'. It was first suggested by a commenter (LB) but here I formally identify it and can use recent moves in the FTSE to illustrate it. This pattern is usually seen after sharp sell-offs and is a sign of two phase base.

The initial bottom is just that, a bottom, followed by a rising body of recovery which encounters the falling humerus, which few find humorous, only to be followed by an acceleration higher in the direction of the forearms, technically called the ulna thrust.

The whole pattern is indicative of anyone who has been long through the move - crapping themselves.

Continuing from yesterday's post on 'Pain in the Hedge’ there have been lots of blow outs of popular shorts and as expected oil things were the most ramped. The likes of bombed out Tullow and Premier Oil are up 50% from a few days ago but even large corporates are on the move in dramatic style. Rio Tinto has busted a lot higher (+8% today). That is impressive for a very large corp that represents everything that is currently meant to be doom - EM, funding, China and commodities and growth. Arcelor is also up 7%. European steel up? It would be an absolute tragedy if SSI, the owners of the UK’s Redcar steel works, have stopped-lossed out off 1,500 UK steel jobs at the very base.

The idea that shorts are causing pain and a good indication of positioning to add to all the other exchange data we see, is a nice chart courtesy of Martin Edlund at Nordea. Macro performance vs MSCI World. This was part of a piece by him actually questioning how long this rally can go on but it illustrates the point I want to make.

Though we are having spectacular rebounds in popular shorts, I feel that resolution of whether we are going further up or down will come in the form of 'The battle of 1995’. This isn’t the year 1995 but the SP500 level that has proven so tenacious recently. It falsely broke on FOMC day (not for long) and sees clusters of various technical levels, the most basic of which is seen here.

The macro outlook may not have changed and look rubbish but the price has and, as ever, money management rules married to price make people do things they really don’t want to or believe is right.

On a different note, it looks as though my car will be recalled by VW. My questions are 1) will any changes effect the performance and economy? 2) If they do so detrimentally do I HAVE to comply with the recall?

So far friends have advised me that the answers are 1) yes and 2) no. If this is the case and I am a typical customer then this recall is gong to cost VW a lot less than predicted as the number of no-shows will be huge. The only thing that would make me get it changed is if my insurance company started differentiating between fixed and unfixed cars or some idiot in government decided my car was no longer road legal though it produces less emissions than the 1985 school bus next to me. Or the Highways Maintenance truck that I was behind last week that had a vat of boiling tar on the back emitting more black smoke than Mount Pinatubo.

And finally finally, I gather that the UK prime minister has announced a project to build more affordable housing. It is to made available to those under 40. AGEIST! The further problem is that affordable housing is traditionally completely rubbish. Tiny shoeboxes that are destined to become tomorrow's slums that any occupant aspires to leave asap. So here's a plan. Instead of building shoeboxes crammed together in maximum density the government should build thousands of spacious 5 bedroom houses each in their own 1/4 of an acre. Affordable? Well they would be if the government built enough of them to drive down prices. Not enough land? Errr.

Pick a green bit.

if you can find one.

-------

End of day update at 21.15 BST - Well fancy that. The SPX closed at, you guessed it, 1995. The battle rages on.

When I hear long term reasons for short term positions being rolled out as long term reasons for hopefully short term positions that finally have to turn into really long term bottom drawer compost heap trades (rotting through carry costs) on now very very long term views (Greece for example, hands up who is still short Europe because one day Greece is doomed) then I take the moves to be positional squeezes.

We hear lots about underweight equities in funds and how big PMs are hedged up to the eyeballs. Assuming that these massive hedges were on the back of the most recent China/slowdown/Fed etc theories then I presume they didn't put them on during the first four days of the August fall. Folks like to digest a monster dump before racing in with a hedge program. So that would imply that those hedges would be put on in the range we are now in for equities. Which would further imply that further climbs from here would mean those hedges are creating underperformance to the index. I don't know any equity manager who likes to be seen to underperform a simple passive index. *

VIX is a good indicator of hedge unwind activity. We are now sub 20 and with that in mind I would not be at all surprised to hear that most of this move higher is pain in the hedges. There is nothing worse than falling volatility and a counter directional underlying move to induce thorn bush, backward dragging, hedge pain. Well, apart from not believing the move and having to cut said hedges for pure money management rules. That's razor wire.

A 85,90, make that a 95 point rally in SPX over the last 30hrs is garnering only a fraction of the comment a similar fall would, suggesting the longest river in the world is dominating the thought process. Denial.

It is interesting how a near 100pt rally in SPX over the last day and half can be dismissed as an understandable move, yet to consider another 100pts higher for the rest of the week is considered sacrilegious and nigh on impossible as it would take us so near to the all time highs. But at current momentum the all time highs are only 3 days away. Absurd? Most likely, but let's get some symmetry into the assumed bear argument.

It also looks like M+A just keeps rolling along too. Never underestimate the power of a humongous heap of cash in the coffers, especially when cash has outperformed your stock and nearly every other asset recently. Fancy a bit o' sweet Symphony for an Alpha bet? (Verve verve voom).

Oh and thank heck for this rally as my FTSE long red hot poker has been replaced by FTSE long soothing balm. This is highest we have been since the August crash, even approaching July lows. Not bad for a commodity and EM laden index.

Or perhaps it was all on the back of the compulsory sale of 5p plastic bags by UK retailers. Got to be some inflation in that move.

*The old maxim - If you want a good hedge, go to a garden centre.

Are you so wrong it hurts? Or were you just so so right with your Fed and NFP calls?

As regular readers will have surmised I am a huge sceptic as to the value of each man hour employed Fed watching and forecasting.

After the latest NFP figure I am hoping that guessing where NFPs will be is also consigned to the same trash heap of wasted manpower. Anchoring of expectations around an average has generated such a feedback loop of self-reinforcement that any deviation from expectation produces swings in response that dramatically outweigh what they deserve. Friday’s NFPs were a case in point. The market expectation was for a figure around 200k and a figure of 140k (a difference of 60,000 people out of 300ish million) has meant that expectations of future Fed rate action has been further pushed back, with the market now expecting that it may not be 'til March 2016 - which suits me as that’s always been my lazy 'uninformed but doing better than all you Fed analysts’ bet.

But you can’t have it all ways. You can’t say Fed forecasting is valid yet get it wrong in September in calling a hike, then shout and rant at the Fed for being so stupid, then forecast the NFP wrong with the actual figure then forcing you to push your Fed calls out to March. Sometimes you gain more respect and even gain a cathartic release, by just saying “I was wrong. Just so wrong it hurts”.

But no nononononononono. That’s as helpful to a career as a politician declaring that they take shed loads of Class As and have a penchant for butchered animal parts. It ain't gonna happen. Instead this weekend's bank research was littered with probability changes. Such as ‘Our model probability for an October rate hike is now below 50%’ Or ‘our base case for a September December rate hike is intact but our bias is for delay’ It’s all completely useless because none of this changed before the NFP was released and we could all see with our own eyes that it was lower than expected and probability outcomes had changed. If you can change your probability with impunity on a horse winning right up to the point it crosses the line then we would all be down at the track looking like gods.

Now even if you could call the Fed correctly that doesn’t mean you get given a cheque to retire on. That call has to be translated by the markets into cash and that is done by having a position in something. Granted, betting on Fed funds and the very short end of the curve is the most obvious high correlation translation of your Fed calling genius into profit, but most of the other stuff really isn’t. You can call the Fed spot on and still have a large probability of losing your shirt if you had put that into an equity index play. As we saw on Friday the NFP was bad enough not to cause any confusion as to whether it was bad or not, it was bad, yet the SPX, after plunging 2% on the falling growth story, put in a turnaround to end up 1%. Knowing the NFP would have been useless for you unless you also knew market positioning and which ever meme everyone else thought more important as we are back to 'Zirp forever buy equities' vs 'low growth falling earnings sell equities' basics. It isn’t easy.

I would also like to remind many commentators that Fed fund futures are NOT the probability of where Fed funds will be in the future. As they are set by the market we can add them to CDS and implied volatility as indictors that do not represent actual probabilities of outcome but market consensus guessed probability of outcome.

The saddest omissions from all commentary this weekend are the apologies. I haven’t yet seen anyone apologise for their rants at the Fed for not raising rates in September, even those who are now saying ‘March earliest’. The whole Fed watching game is a game and I am hoping that the market will be getting bored with it and moving on to making investment decisions that aren’t based on 0.0025 of principal.

Market from here - As per my last post I am still long FTSE things as it best encompasses all round risk bounces in DM, commodities and EM. I am fully aware that technically we are not yet out of the woods and I am equally aware of all the reasons for not being long which everyone who is short is screaming at me. When they are no longer short I will listen again.

It's that time of the month again when reasoned thought is replaced with illogical emotional outbursts and shouting and tears. Where how we feel over something that really doesn't matter THAT much in context, damages our relationships with others, but it will all be forgotten again in a week's time. Yes, it's NFP time when the market sloughs off another month of old jobs data in a histrionic fit of over concern.

NFP, the kitchen sink of data sets. Whatever your core view you can tie it to the NFP or, failing that, one of it's components as there's always a component to support any argument.

So fo all you NFP guessers I am recycling the NFP calculator I first published on Macro Man 18mths ago. Easy to use, just in your max and min and the algo will do the rest

I have been travelling to places where the real world appears a million miles away, where legions of white shirted chino clad lackeys are testament to the trickle down effect of economics, as they are all ultimately supported by the whims of a few billionaire’s. We may prefer them to be working in hospitals, but those not smart enough to occupy frontline medical care posts have to earn a crust somewhere and why shouldn’t it be in flogging the finest toy, such as a submarine, for your superyacht? Interestingly I sat next to an explorer-cum-investigative journalist on the plane out there who has taken these incredible toys and is using them for global environmental projects. These projects are also funded by the rich and famous. So something good does come out of techno-plaything development. Much as our cars today have design features developed by Formula 1, our environmental changes are being monitored by technology spawned from fun money. Ok, I know you are thinking it, so lets jump to it - does that mean that emission test rigging software started in Formula 1? Errr... No idea. But I can tell you that if you are concerned about emissions then I bet the VW NOx emmisios are dwarfed by the output of the words shipping fleets. To put a bit of emmisions perspective on it -

With VW - The company admitted the device may have been fitted to 11m of its vehicles worldwide. If that proves correct, VW’s defective vehicles could be responsible for between 237,161 and 948,691 tonnes of NOx emissions each year, 10 to 40 times the pollution standard for new models in the US. Western Europe’s biggest power station, Drax in the UK, emits 39,000 tonnes of NOx each year. (The Guardian)

Meanwhile shipping around the EU’s coast alone -

In 2000, in the seas surrounding Europe (the Baltic Sea, the North Sea, the North-Eastern part of the Atlantic, the Mediterranean and the Black Sea), sulphur dioxide (SO2) emissions from international shipping were estimated at 2.3 million tonnes a year, nitrogen dioxide (NOx) ones at 3.3 million tonnes. (http://www.transportenvironment.org/what-we-do/shipping/air-pollution-ships)

NO2 is not pleasant but NO? No, you are having a laugh. They give it to birthing mothers so it can’t be that unsafe. Which also leads to my hypocrisy flag being raised from the touch lines when I see campaigners trying to ban the recreational use of the stuff because a few people have suffocated on it, yet still alcohol is tolerated by comparison.

Now here’s a thing I cant marry up. Read everything financial and you would believe that the world imploded in August and is is now in a very very dark place. But we are seeing divergence here. Not EM vs DM divergence which normally doesn’t last long, but in this case it’s with us financial lot and the rest of the working population. Now I know that Redcar in the UK has just seen a nasty set of job losses associated with the fall of commodity prices, but everyone else I talk to outside finance seems to be getting along just fine. Even the village I live in was a veritable ghost town/village this summer as surprising numbers had gone off on foreign holidays. These may have been booked back in happy January, but the mood on the street still seems pretty upbeat, with restuarants full and people still happy to pay £5 for a bowl of cereals (unless it contains traces of paint bomb). Folks are even still buying oil, as the price, despite the $20 calls and gloom ahead, still tracks sideways. Even the Chinese consumer is getting more confident.

So who does the Fed listen too? “ Well on the one hand… and on the other…" As usual the shouting is loudest from those who disagree with things and the Fed and central bankers are easy game as they rarely shout back. I, for one, am very happy with rates staying low as I have a base rate fixed mortgage and am willing to swallow my academic pride in reasoning for higher rates in return for the selfish payoff of lower monthly outgoings. I wouldn’t be surprised if we are seeing a ‘Tory polls' effect in interest rate forecasting either. Where the Tory vote was probably underrated as it was seen to be immoral to vote Tory, but the actual selfish vote pushed the tick in the box that way anyway, I will stand up with the economic intelligentsia and proclaim ‘INTEREST RATES SOULD RISE!” yet muttering under my breath “Keep 'em low, pleeeease keep 'em low”. Which is how I imagine many at the Labour party conference are feeling as they cheer on comrade Corbyn in a sign of career preserving gusto whilst really thinking ‘Please Lord, make the man see sense and not carry out half of what he is threatening’

Whilst we are on Corbynomics I was just reading the fact check on his speech here https://fullfact.org/factcheck/corbyn_speech_labour_conference-48468 And it brought up a fact that includes an assumption, or rather doesn't include a fact, that sorely twists the truth to the point that it may be clouding important data.

“1 in 7 of the labour force now work for themselves… They learn less than other workers. On average just £11,000 a year.” This is right, according to the Office for National Statistics. Its latest figures show that just over 31 million people are employed, of which 4.5 million are self-employed. That’s around 14.5% of all workers, or one in seven (measuring over May-July 2015). Its figures show median income from self-employment was £207 a week in 2012/13—which would be £10,800 for the whole year. It hasn’t published a more recent update to this analysis.

There is a magical figure in being self-employed within a one man Ltd company and that is £8,040 per year. This is the maximum that one can earn without paying additional National Insurance contributions but receive NI benefits and whilst staying below income tax thresholds. A self employed person has various means of taking income out of his or her company and taking a salary is probably the least efficient. Though the tax man frowns on it, self-employed folks have a bias to maximise their dividend payments as tax on dividends is zero, the only payment is the 20% corporation tax on the pre-dividend profit. This is lower than the NI and income tax associated with taking it as salary. This may change next year with the government raising the tax on dividends to 7% - a cunning wheeze to stop such loopholes being exploited which will cause many to move to regular salaries thus pushing up the earnings data and 'wage inflation' data next year despite income actually falling due to the tax increase. But the question is where does the statistics office derive their 'earnings' figure from? I have a strong suspicion it doesn't include dividends and, if not, all earnings figures are being skewed downwards, especially as more and more people are becoming self employed and substitute salary for dividends. Corbyn has used this skew in his favour with this fact. Earnings do not equate to income.

But now let's meander back to credit markets and interest rates. The attack on credit by the markets has already started as thoughts of slowing growth and Fed tightening (err does that tally?) identify leveraged slowing companies as the weak point. The weak point near the hinge of the oyster where you jam in the knife hoping to pry it open to reveal the gloopy mess inside (few have pearls). But as with most oyster openings, fingers will be lost. I find it interesting that so far, it isn't the Fed taking away the punch bowls but the markets. In effect the market is acting like a Fed hit-man; removing credit and killing weak companies without the Fed having to do anything. Like a Mafiosa boss, the Fed just has to hint at what it would like to happen and Mr Markets and the boys go and do the dirty work getting rid of the weak. "Wasn’t me officer, I didnt raise rates. I was miles away when they suffered a credit squeeze and I can prove it - Just read the minutes”.

But back to markets. Despite whatever I have thought and do think, equities have played out a classic fall-wedge-fall pattern and I am hurting in the FTSE department. I have been to the doctors and they say it’s due to me being an out of touch with the "new now" and apologise for not having the medical specialism to remove the red hot poker I am currently entertaining in the nether regions. I will continue to bear the pain and though Dr. Market sees no hope in my recovery, I will take some comfort from the fact that markets appear to be at an ebola stage. There have been deaths and will be some more but this downturn isn't going to wipe everyone out despite current prognostications.

Whilst I wait I'll do what most people do when they are suffering and that is to make it fashionable. Just as they have with living in tiny shoeboxes, not having any possessions, wearing over-tight trousers (I also wear over-tight trousers but they weren’t when I bought them) and having itchy facial furniture. The battle of Shoreditch was therefore all the more entertaining to observe as it was fought between two tribes, one who pretend they don’t have anything and want to keep it that way, and the other who don’t have anything apart from i-products and want to keep it that way by forming an inefficient cornflakes and gin based economy.

So let it be known that the most fashionable position in the market is therefore to be long and wrong. But not morally wrong, No! For morally it is only right to support our industries and the hard working who strive to lead better lives. Morally it is better to be wrong in the eyes of the evil market .. Oh bugger it - I can’t keep this politico-moral stuff up. I’m off to buy a pair of skinny salmon colored jeans and by a bowl of cereals, if only I could afford them. but before I do here is some light amusement courtesy of Mitchell and Webb with their take on the introduction of new technology. I assume we can read stone as 'pie 'n' mash' and bronze as 'cereal and gin'

And thank you @kentindell for bringing that to my attention.

The fixing of emissions by VW strikes me as comparable to bank fixing scandals.

The rules were in place but, as with any regulation, the industries effected do their utmost to play the rules to their advantage. In the case of VW they were obviously hoping that the rules meant that their cars had to pass the test rather than perform to the test outcomes permanently. They adjusted their behaviour to pass the test rather than observe the essence of the regulation.

Now call me a cynic, but I find it hard to believe that VW were alone in this practice as many car manufacturers produce similarly impressive figures with engines that are no more advanced than VW’s. Much as the LIBOR or FX fixing or PPI misselling scandals provoked industry wide investigations and fines I would not be at all surprised if the VW case initiates the same within the car industry.

VW stock has been crucified and the reputation of the company sorely hit, but the cost to the business is going to be comparative. Buyers may move to other brands if emission tests results are recalibrated and the outcome makes VW’s uncompetitive, but that assumes that the competition is untouched and not equally branded as cheats. I would not be surprised that if VW go down for this they will try and play a whistleblower role (as bank dealers do in financial scandals) and take down the competition too to keep the playing field level, all be it at a lower level.

If the banking model is anything to go by, the HQs of all global car manufacturers are going to be hives of desperate activity checking that a) they haven’t been doing the same, b) if they have, trying to bury the evidence or backtrack (can they really remote hack car software and reset it?) c) Contain the fire by finding internal scapegoats, firing them, offering them up as sacrifices to the judicial system and then declaring that they have put process in place to insure it will never happen to them and all is good.

To be honest I don’t care too much if my car burps out more NO2 than declared in a test as long as I am street legal and the low running costs I am enjoying don’t change. But the tax man certainly does. I may decide not to buy a car if it jumps up a car tax band due to emissions but if the taxman has been defrauded out of billions due to cars being declared at a different tax band to where they actually lie then that is as good as fiddling your tax returns. The pollution issue is minor compared to what happens when you defraud a tax authority and this is where people go directly to jail.

But it doesn’t stop at pollution emissions. I also understand that sound emissions are as important and only just found out that the cool opposite mounted twin exhausts on nearly every car these days has nothing to do with performance cosmetics but sound emissions. And even there the firmware in the car detects the sequence of manoeuvres synonymous with a sound test (the distance of the max acceleration, the pause distance and number of repeats) allowing it to adjust for the final test sample.

The one test that we all have questioned for years (the one we are all most selfishly concerned with) is the fuel efficiency. I am sure that you have to weigh only 10kg and drive the car full of helium along a steel road using solid titanium tyres in a vacuum to achieve some of the published results.

The level of fines being imposed on large corporates is just eye boggling. I am not sure that car manufacturers will become the next ‘banker’ in the eyes of society but this VW Exposé does little to enhance the reputation of Big Corporate. I do wonder if there comes a point where it just isn't worth being a big corporate. Private employment is seeing a growing trend of freelance and self employment, with groups working as collectives or hive minds of efficiency, so perhaps there is case for huge corporates becoming collectives of small companies. It would certainly make it harder for the regulator to pin a massive fine on them as they would be behaving as a swarm of bees rather than an elephant. Any component being fined could be sacrificed to bankruptcy and a new one grown using a lizard tail philosophy. I just don’t know where that point of efficiency lies.

And it has correctly been pointed out to me (first comment below) that car tax is CO2 dependent not NO2. Know your pollutants. But I still bet every aspect of testing and firmware will be under investigation. Standing by for engineers incriminating chats to hit the wires.....

Opinion is split over the Fed decision though I would suggest the split is not even.

My first thoughts were -

- If the Fed were FIFA there’d probably be an investigation going on right now into emerging market bribes.

- It's paradoxical that the market moans that the Fed is influenced by the market and then the market moans that the Fed hasn't done what they want.

- Fed cut volatility.

- Perhaps instead of weening the market off low rates the Fed is trying to ween markets off Fed credibility to make it's own damn decisions via the rest of the curve.

- As with China and Greece, 'Fed risk' has to be moved from the acute ward to the chronic ward.

An event risk has just passed and the immediacy of imminent doom slips back and any belief you have as to the long term outcome has to be moved out in a smear across weeks rather than days of future ‘maybes’. The risk may be ahead but it is no longer today. The bears will be arguing that the end of the world may not have occurred today but it damn well will soon and the bulls will be breathing a sigh of relief for now.

Yes OK, but I think we can squeeze in a quick holiday before we have to sell the cat.

But what for positions? As mentioned in Tuesday’s post, the most likely outcome is a fall in volatility and we have seen it coming off pretty hard over the last 2 days. But to expand on that, a fall in volatility normally invokes a period of 'carry creep' where if nothing is going to go wrong right now, yield starts to dominate as the cost of carry erodes shorts on yielding assets. In other words risk assets grind higher and, with the bear call so dominant, a grind higher will be accompanied by wails of pain and disbelief,

Watching the price action in that uber-benchmark of SP500 has been fascinating since the announcement. Up, down, up, down and as with all roller coasters each oscillation is accompanied by whoops from those on the ride, but the ride ends where it started. So far SPX is within a gnat's crotchet of where it closed yesterday. Interesting to note that the extrapolationists are having a ruler snapping time trying to call the next move with the intraday movements being so wild, but a low close sees the majority calling it lower. Because it closed lower. I am also aware, having been reminded by @NicTrades, that 'a red market on Fed day usually means follow through the next day'

Technically speaking the 1980-2000 SPX area has encompassed a myriad of important levels and to see the blow to 2020 can lead us to assume that many stops where taken out leaving us room for a resumed fall.

But there is a piece of the jigsaw that needs to play out first and that will be Asian markets overnight. Lower for longer US rates ‘should’ be of assistance to all those Emerging Market countries that have been listed as being most damaged by a Fed rate rise (most of them). With Asia woes having been a major driver of sentiment recently it makes tonight's moves all the more important.

Nothing is easy re markets, but the Fed is back in the box for a month though I note that Octobers have a tendency to provide market and hence confidence jitters that could give the Fed another reason to delay.

For now I am going to sit back and brace myself for the deluge of articles telling me why the Fed was wrong. On that note if someone comes across one praising them can they send it to me?

Update 18/9 11am BST - Looking at this morning's price action I think we have stumbled upon a new market's circle of life.

Fed steady -> EUR/USD up -> Dax Down -> DM eq down -> OMG -> Fed steady

It’s a bit like going along to a sports event that you have no interest in just because all your friends are going. Or a dinner party with the people that you really can’t refuse again as you’ve run out of excuses. Or the christening party of a work colleague’s child.

Today sees an event that I have no interest in, yet all my friends can’t stop talking about it and want me to join in. As with soccer talk, by the way I am rubbish at soccer talk, the greater the detail of knowledge expressed by a follower, the greater the self-perceived standing of that person. But knowing the maiden name of the goalkeeper’s maternal grandmother is not going to change the outcome of the game. And, I am afraid, knowing anything about the thought process, economic inputs, outputs, shoe size, dietary requirements or star signs of the board of the Federal Reserve will make absolutely no difference to the outcome of today's meeting.

We are all spectators watching it on TV and whilst we may think that our jeering and shouting at the players on the screen will make a difference it will not. If we all switched off and went to the pub with our friends there will still be an outcome without our input. As my wife told me, "only worry abut things you can change”. I cannot change the outcome of the Fed’s decision.

So what is all the fuss about then? Well the function we can change is not the decision, but how we maximise our gains and minimise our losses against the uncontrollable outcomes of the decision. The options are simple -

1. Take a view on the Fed, mortgage the kids and load the boat. 2. Reduce your risk to zero and go to the pub. 3. Do nothing but pre-write two paragraphs for your next report

i) Lost money due to unforeseen and blatantly stupid Fed action.

ii) Made money due to exceptional skill in reading the Fed decision based on knowledge of board members shoe sizes and grandmother’s maiden names.

For some there is of course option 4. Not to personally give a damn as you have no positions or skin in the game, but go on and on and on about your opinion in the hope that should you be right someone will pay you for your opinion next time.

Human nature hates uncertainty, markets pretend they hate uncertainty but actually make all their money from it, and journalists just love it.

(By the way, if you do happen to be a Fed Board member reading this, just email me direct and I’ll explain why my stalking of your daily routines and habits should mean you do what I think you should)

I’m back from two weeks of bliss on a boat. The holiday was disaster free and ranks as one of the best ever. Croatia is a dream and remarkably we found it cheaper than Greece. Yes I know that there are places in Greece offering normally priced coffee but my ‘Quayside Coffee PPP’ indicator saw Greece at €3 and Croatia at €1.50 this year. Boat stocking supermarket trips were also considerably cheaper, probably due to easy access to Croatian national hypermarket chains rather than village stores. Dining out was much more varied too, Croatia providing a wider selection than the predictable Greek offering of 20 identical quayside tavernas with identical menus. Where Croatia does gouge it’s pound of flesh over Greece is on mooring fees. Greece considers the sea and access to it a basic national right so town facilities are free. Croatia bill you handsomely for securing your boat to anything. But enough of tourist micro-economics.

I am pretty sure that the high US employment figures can be explained away by the number of people employed to comment on future Fed action. I feel like a philistine in expressing the view that I find it all a bit dull. It can be compared to watching a Shakespearean play where the cognoscenti exhibit their literary prowess by laughing just before the clever witticism occurs, instead I’ll just laugh after the event when I've had time for it to sink in and understand it.

China - Down, down, deeper on down

In basic terms this is why the world is terrified.

The site also states that "...the country has consumed more concrete in the last three years than the United States did in all of the 20th century". A fact I haven't checked but find jaw dropping.

'Nuff said on China. If you want clever insight read George Magnus - you can find him on Twitter @georgemagnus1

It would appear that the markets are now bracing for global recession with the BAML survey creating stories such as this 'Fund managers braced for global recession' http://on.ft.com/1NuGgxr

Which has me assuming that 'braced' means 'positioned'.

Sentiment measures on SPX are also flashing 'it's in the price' (H/T @NicTrades)

In which case we are back to the most basic market game of trading the expectation derivative of expectation of expectation.

But a couple of things have happened this week that make me go 'uhhhm'. The first is related to the anatomy of a crash. When things get nasty everything starts to correlate in a nasty way with regards to down moves. Pretty obvious really as the perceived cause of global disaster is watched by 'Macro Tourists' as the trigger for moves in all other markets. Though correlations are still high relative to long term averages , they are starting to fall.

When I went away every move in Chinese stocks was being shadowed by Developed Market stocks (in particular commodity stocks), yet over the last couple of days this relationship appears to be waning. China had a hefty dump on Monday yet DM markets appear to be shrugging it off. Indeed the techie sector is now even threatening to break upwards through some interesting levels, all the more interesting if you look at the Nasdaq super-low sentiment level in the table above.

Can I read this as a sign of short term punter ADHD? I could try and rationalise it by suggesting that if you were going to get short on the China story you would have done so by now, having had a few weeks to sell rallies and, of course. believing that this is 'the big one' you wouldn't be waiting for a massive rally to sell into.

The volatility market is still making headlines with remarks being made as to the shape of the VIX curve and the VVIX vol of vol. There comes a point where trading the derivatives of derivatives starts to cause ripples in the deep space of price complexity that becomes detached from the actual here and now of the basic price. Much as using the Hubble telescope to study oscillations in binary star systems billions of light years away may give an insight into the weather next Monday and therefore to umbrella sales but it is more likely that umbrella prices will be more dependent on how cheaply China can make them.

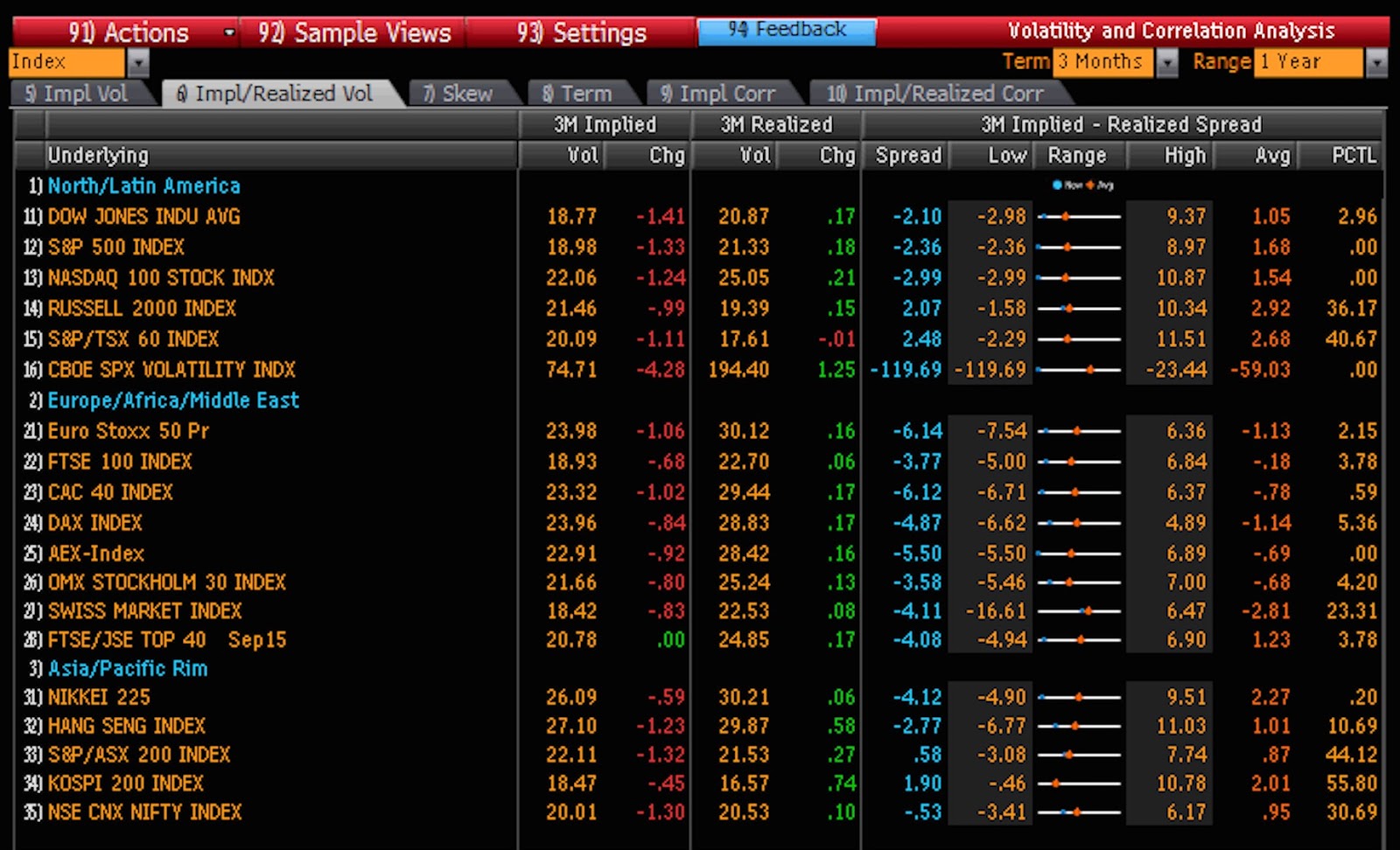

But the most important thing to remember and mistake not to make, is to recognise that implied volatility is not actual volatility. The VIX et al are measures of perceived future volatility derived from the prices people are willing to pay for options. Actual volatility can be very different. I have a feeling that though implieds are running hot at the moment they are about to be undermined by a fall in actual volatility. A further point is that historic volatility, which is what actual volatility was (not is), is not present actual volatility.

Currently implied vols in major equity indices are trading lower than historics in the 3 months. (thanks to @BrokenBanker for the Bloomberg screenshots)

But this doesn't mean that the implieds are too low. It just means that people don't think we will have a blow up similar to August's any time soon. Historic volatility, by it's nature, lags. It's effectively an historic moving average. If it is announced that a currency is to be pegged in a week's time the historic would not reflect the fact that volatility will be 0 until the historic period expired, whilst the implied would probably fall, but not to zero as players would be betting on the chance the peg didn't happen or would blowup, whereas the actual volatility would be 0.

My general point is that using volatility as an indicator is a minefield unless you know exactly what you are looking at. Implied volatility is partly volatility but mostly a huge chunk of estimated probability. Just look at volatility pricing in the USD/Saudi Real which has a volatility of near zero. As with CDS, volatility is crude tool for financial journalists to twist stories of woe from.

We all like to yell and scream at high intraday volatility but the best way to defuse the panic is to apply moving averages. Below is the SPX with 2(green) 5( grey) and 10(red) day moving averages applied.

I know I should be using fibonacci numbers as they are apparently magical but looking at the nice normal 10 day (2 week) we can defuse the whole of September's moves back to 'remarkably dull'. I am predicting that falling actual volatility will undermine positions in implied volatility and with it a reverse pressure on the risk parity funds that have been so cited for vol following trades, to actually start buying back.

I am still not playing the 'it's all going to melt by the end of the week' theme even with the Fed in play.

Oil - There has been a renewed call fro analysts that $20 oil is on the way again with Goldman joining the fray. The last time this happened we saw the base (Shakespear's oil bear witch project). We also have another signal. The tabloids are calling for £1/litre petrol in the UK yet the oil chart doesn't exactly say 'dump' to me.

The majority of assumptions are based on the continuation of trends and that is why so many are wrong.

One last thing - There is a very good WSJ series on Tom Hayes and his case the third instalment of 5 being here - http://graphics.wsj.com/libor-unraveling-tom-hayes/3. the march of the regulator continues and I continue to suggest that if the transparency on pricing demanded of financial institutions were applied to the rest of the retail sector then UK High Streets would, far from being rejuvenated, have to be refitted as jails.

*For financial regulatory news and updates on current cases I recommend following @NewLeafAdvisory on Twitter.

For the next couple of weeks I’ll be away trying to spend a relaxing time with my family sailing in Croatia. I’ll be acting the part of Captain Bligh as I run a tight ship and don’t expect any mutiny. To be honest the kids, though they pretend that all they are willing to do is sunbath and drink the ships stock of rum, are pretty reliable when it comes to handling the boat, so it should be a lot of fun. Going away with two other sets of close family friends, making up our own mini-flotilla, guarantees camaraderie and fun for all generations.

Although it could go wrong, I'm hoping it turns out better than it did four years ago. If you want to read just how badly that went, read this - "What I did on my holiday" .

- Oil is up over 4%6% wow, now 8% as I write. As stated at the beginning of the week, energy, commodities and all of the other bombed out components of recent moves need to reverse to confirm that this isn’t just a flash-in-the-pan equity bounce. This oil rally is the sign. Indeed oil is even looking has broken its death slide trend that started in July.

- My TDI signal has just triggered. Yesterday my taxi driver said it was due to China slowdown. I wasn’t sure what was due to China as I wasn’t listening to that bit, only being triggered into awareness by the ‘due to China slowdown’ bit. Which was followed by a comment on oil prices. the Taxi Driver Indicator is a time honoured indicator of mine which has wonderfully predictive turn calling abilities and is used to confirm the 'Gone Tabloid' function, which in itself follows on from the "Armchair General Indicator' which the BBC's economic journalist Robert Peston triggered on Monday.

- Liquidity. My views on why illiquidity driven moves are as much an opportunity as trouble have been previously published here.

-VaR. If everything told you that the bottle of whisky I was offering you was genuine and you knew that the only reason I was selling it to you for 10p rather than £18 was because I couldn’t fit it in my flight luggage due to weight restrictions, would you refuse it because the price had just moved 99% lower so was very likely to move another 99% against you? - Because that is exactly what using value at risk (VaR) models results in. Just when you want to buy value, your volatility driven model says you can only buy a tiny amount.

As a quick aside I was pondering setting up a fund with a reverse VaR function and seeing how it got on. Of course all the fund consultants and allocators would have pink kittens at the very thought of allocating to such a fund, but I have the killer reason for them to do so - diversification. Diversification has kept many an appalling performing fund alive and I bet there aren't any funds out there offering diversification of risk in risk. (Make cheques payable to....)

Data - The data coming out from western economies is pretty strong. Though the market is anticipating a massive slowdown caused by China it isn't here yet and if it is anything like predicting the Fed, any interpretation of the future will be made irrelevant by new information emerging before the event arrives.

- Equity indices are through their original dead cat bounce highs. But expectations that this is just a bounce dominate. Expectations of SPX hitting 2050 again in the next 2 weeks appear minimal (update, well they might be now). The shake down we have just seen never had all the ingredients needed for a full scale collapse. The recovery in oil and commodities is solid and new ultra-doom calls based on China will most likely, as with Greece, need to be put back on the shelf ready to be brought down as bear food to justify any subsequent falls. China and Greece may be chronic but they are not acute.

Where are we? I don’t think the anatomy of this crash is truly crash like. Granted, we have China and commodity stories, but the part of the equation that doesn’t fit for me is the mood. Post financial crisis the mood has been one of perpetual doom with an expectation of each subsequent crisis being observed as ‘the big one’. Yet they never are. The last few years' stock rally has been the most fought rally I have ever observed. I still find it hard to believe that we are due a really big correction until we have had the exuberance phase where exuberance has leverage in tow. If something is believed to be such a sure fire bet then it is worth mortgaging the kids for.

Yes, various sectors have seen prices pushed to levels that are hard to justify using normal metrics, but they have not been employing enormous leverage. The rally over the last few years hasn’t so much been so much one of exuberance but more of one of reluctance driven by a desperation for yield.

Here's a map which represents the classic phases of an asset price.

We can ooh and aah at it and instantly suggest that it represents the Chinese stock market pretty well

But where the Chinese and Western stock markets differ is that the Chinese market went through the mania phase with leverage being prolifically employed by the general population and many a Chinese taxi driver piling in.

Western markets have not enjoyed the mania phase and general public leverage into the stock market is not being deployed. I have had it rightly suggested to me that the 2007/8 crash didn't see a stock mania before crashing, but it did see massive leverage unwound from society and the destruction of money in circulation. All crashes involve the unwind of leverage but there is little evidence of leverage in the stock market and I would imagine there is dramatically less after the actions of this week.

Instead I am suggesting that we are only at the bear trap in the 'awareness' phase of the map. We have the mania, leverage and completely stupid stock boom ahead of us.

I know that this is a pretty punchy call but the more derision it receives the more evidence I have that the market is not thinking it, let alone positioned for it.

The China meme has sucked in macro tourists and armchair generals and we know we have peak armchair generalness when Field Marshall Robert Peston BBC TWT(bar) takes to the field telling us how the world's biggest calamity has emerged over the last 3 weeks. 'Tail end Charlie' research units (those who are last to notice a change that they have to follow and are more concerned with following herding biases than being first with an idea) are now calling Chinese recession where four weeks ago everything was fine. Not saying there won't be, but the flip of opinion over the course of three weeks with respect to long term forecasts, that should be influenced by slow changing indicators, is laughable. There has been a polarisation of opinion with regards to China (the root cause of all this).

Some look for resolution of the fight between the 'buy the dippers' and the 'doom 'n' gloomers through watching the stock volatility index (VIX) but I am watching all the usual culprits and oil especially. To get a really good 'muppet bottom' the whole lot should go up again, commodities, equities, HY, the lot. They haven't yet and so I'll leave fine tuning VIX micro trigger levels to the quant gurus and take a higher top down view. If this is make or break we can afford to lose the odd 3% of move for the sake of information resolution rather than trying to be point picking heroes.

I have some very clever friends who are telling me this is the start of a new economic phase and that China is having its own 1929. Not just those predictable overlay 'these look similar if I change the scales' charts, but in society's overall investment and development phase. I have sympathies with this but the problem, as ever, with China is that it is so hard to work out what is really going on there. Which makes me laugh all the more as we are getting some exceedingly detailed prognostications over not only China's outcome but the 3rd derivatives of it in individual Western stocks.

Should I be fading consensus in a market where we can't be that sure what is really going on as I also cannot know what is going on? Well yes. Probably more surely than in a market where I know it is easy to see what is going on and it is only me who doesn't know what that 'going on' is. If the majority of people bet that the next lottery draw will be 17 36 02 28 13 04 it doesn't change the odds of it coming up and I will happily bet against their guess being the result.

Price is rubbish, volatility is killing VaR models and the reduction in risk and willingness to establish positions, when the variance of perceived value to priced value can be so huge, means that liquidity vanishes. The 50 points SPX fall in the last hour of trading was a good example. What was that due to? News? Not that I saw. Some change in the economic outlook of everything? Don't bother asking an economist why the value of everything has fallen 10% versus fiat cash (now there's the irony) in the last couple of weeks as you will know that everything that follows will be rubbish.

These markets aren't for economists as they are too fast moving. The best economists can do is to take the prices that you yourselves are creating via market actions and input them as fast as they can into their own models to predict new prices. Which is pretty irrelevant as the input prices will have changed by the time that they have done so and you will have stopped listening to them. Economists, like trading models, do fine as long as there aren't any sharp turns in the road to upset the predictive powers of their rear view mirrors. These markets are for psychologists. The brave and the bold will turn out the winners. These are the markets where realising true value and taking the position with little heed to traditional VaR measures will lead to gains and also to more stable markets.

There has been a lot of complaint from the buy side that banks are no longer there to provide the liquidity the markets need, the banks having reduced their proprietary books. But lack of liquidity being due to books having been reduced is only part of the reason. A bank trading book does not provide you with liquidity unless it is willing to take on your trade and it will only do that if it doesn't price the way you do, otherwise whenever you will be wanting to sell so will it.

So I postulate that the real missing ingredient here is diversity in trading and risk management style across the whole industry - banks and fund managers alike. With a standardisation of risk and trading models everyone will tend to want to do the same thing at the same time. What we actually need, to add liquidity and normality to the markets, is a return of the old fashioned trading god. The superhero who would stand in when a price reached 'stupid' levels and pick it up with both hands rather than selling more because the money management model is telling him to reduce exposure, even if it is at stupid levels. Investment banks had their gods, Morgan Stanley and Goldman Sachs rates desks of the 90's had characters of whom films are yet to be made because they were too savvy to have themselves publicised. But these days the model is king and when things go doolally there is no sensible hand to steady things. The only hand expected being that of the Central bank. Oh pity the nannied generation.

Yesterday all my troubles seemed so far away.

Stocks looked as though they were here to stay.

Oh, I believed it yesterday.

Suddenly, I can’t sell, there's no liquidity

There's no bid left in the S+P

Oh, hell, we need some new QE.

Why it had to blow, to new low, on my display

This damn model's wrong, now I'm long from yesterday.

Yesterday, 'long' was such an easy game to play.

Thought it was just some gamma decay.

Oh, I believed the bounce today.

Why it fell so low, I don't know, I’m in dismay

I marked risk so wrong, now I'm long from yesterday.

Yesterday long was such an easy game to play.

Now I need a place to hide away

Before they call the FCA

-----

Still holding tight to that long.

The only thing I can report of joy was the meal that I took the family out for this evening as way of taking retribution against the markets. It has been a while since I last mentioned dining establishments, the last one being to slate Aqua Nueva in London, but it is time I redressed the balance.

I have just enjoyed the best meal I have had for years and years. To be honest I wasn't expecting it, even though the establishment does have a Michelin star, as I thought there was only so much you could do as a fish restaurant. Boy was I wrong. Go to 'Angler', near Moorgate in London, for their tasting menu. I was blown away. I'd like to say tell them 'Polemic' sent you, but they wouldn't have a clue who that is, but you could try.

Price is news. And with it is the retrofitting of all news to the price. Has anyone found any news that doesn't base itself on price? What is the news other than price over the last week? Chinese PMI Down, US retail sales disappoint. Is that really worth $5trillion of global wealth wipe-outs? Note here that once again the S.I. unit for stockmarket falls is $s of market cap lost, whereas gains are mere points or at best %s up, if commented on at all.

It would be a fascinating experiment to be able to deprive analysts of past prices (using a 'Men in Black' memory erase flashbulb device perhaps) and see how they get on. Hard enough with stocks, but nigh impossible in FX, Gold or oil where the theory of infinite equilibriums appears to hold true.

If I were to lay the comatose market patient on the table for diagnosis or confirmation of death, I would see a body riddled with price gun shot wounds but I would be looking for the real cause of the problem. That tiny pierce mark between the toes that could signal poisoned injection, the cherry pink in the cheeks pointing to carbon monoxide poisoning or the high radiation count of polonium 210.

Because though the cause of the falls is apparently blindingly obvious, I am afraid that this market doctor doesn’t buy it. Well not all of it. Yes, the riddling gun shots from the assembled uzis of the market drive buy shooting are not to be ignored as a contributing factor, but those are a consequence of the cause not the cause of another cause.

A year ago I posted a master plan of how this could all pan out painting a picture of one last hyperbolic spike in leveraged risk with equities going ‘taxi driver’ long. The end game being one more huge collapse in everything that will be the test of the CB mettle and leave them resorting to real money printing rather than this QE smoke and mirrors type. Or ‘Corbynomics’ as we will now call it, named after a potential UK opposition party leader.

This morning I have been deluged with evidence as to why this market collapse is the big one. It is different, the world has changed and the expected collapse is here at last. But the reasons being offered are old wounds and depend on who you ask, as whatever reason that person ever had for being bearish is now encapsulated in a ‘See? I told you the markets would fall because of x’. Yet nothing has actually changed over the past couple of weeks to justify most of those reasons. The reasons have been there for the last 3 years so don’t come running to me now saying told you so for explaining the last 3 weeks price falls.

Yes I think we know where I am going. All clues to the current diagnosis point to asphyxiation and asphyxiation demands that airways are cleared. And there,wedged down the right bronchus, is a lump of Char Siu. No matter what your tin foil beanie reason for the current market collapse it all actually rests on a market belief that the Chinese State has lost control of its economy and that economy is about to collapse and take the rest of the restive world with it.

But the anatomy of the markets is really not weak enough to see this choking kill it.

- The banks are in a better shape than they were.

- US rates effects on EM debt should have been unwound from a month ago as Expectations of a September rate rise fade

- The call that equities have run up from 2009 lows by history breaking lengths of time ignores that that measure is being made from history breaking lows. Just take your base back to 2007 and stock markets are not at all overpriced. 8 years of no growth in the FTSE value is almost historically low.

Most importantly, the market has not been through a hyperbolic euphoria. A 'taxi driver high', where everyone is long equities and risk. This chart of macro and CTA exposure to US equities as we go into a fall is not conducive to it being a major event. They were short into it. Markets need to be long to be properly wrong and they weren't.

I have also had debates with colleagues and friends into the psychology of today's traders and risk takers. Their argument is that the current generation have been brought up in a world where prices only go up and so are geared that way. I disagree. I still feel that the current generation have been programmed by disasters and are always over-positioned for fat tail events. They all want to be the next Taleb. There may be stability in the crowd but there is no glory. I drag Twitter and social media in general to the witness box. Want to make me a price on the ratio of 'buy it, everything is good' to "sell it, it will all go wrong' posts? I don't know for sure but I can have a good guess.

There is chronic disease out there but chronic diseases are not swift killers and this market doctor is pronouncing that after a Heimlich manoeuvre to expel the Chinese concern the rest of the markets will recover.

This is a misdiagnosis of the 'big one' and rumours of the market's death are exaggerated. But if you do think its the big one then you should be selling US treasuries as Asian reserves have to be unwound. If you don't think it's the big one then you ought to be selling US treasuries for a risk rebound.

Yesterday was a towel chucking day in commodity land.

Oil did it again and I hold up my hand with regards to getting oil wrong as that held up hand is devoid of fingers. The kevlar gloves, donned last week when buying for a bounce, provided no protection from the falling knife of prices.

Glencore shares melted yesterday too along with most other miners. 'Caught out by fall in Chinese demand" said the head of Glencore

He also goes on to blame the price collapse on hedge funds pushing prices to unreasonable levels. HOHOHO Kerbonk (Laughing my head off). Glencore is more hedge fund than most other hedge funds. But as always profit is genius and losses are someone else fault. In the same way as you never hear a corporation explaining away surprise profits through lucky moves in FX, though the reverse argument is often used.

So how many corporations are going to be looking at their balance sheets for Kazakh Tenge exposure this morning and hoping to find a small nugget of exposure on to which to kitchen sink all their management filings, as the Kazakh Tenge devaled 20% overnight? This has caused many shops to close for the day as they convert the devaluation into pure inflation by repricing everything accordingly. Do you really want inflation? Ask a Kazakh how it feels.

Kaz Minerals shares quoted on FTSE up sizeably (even priced in GBP) on the belief that this deal will give commodity producers a shot in the arm.

Not so sure how long that will last as a devaluation is identical to giving your workers a 20% wage cut, and like a wage cut they either take it, or demand more pay. But you have to take your hat of to them that was one hell of a devaluation at making China's 'deval' look like a rounding error. With the vietnamese Dong 1% softer too after manipulation by its CB, perhaps the headlines should read 'Emerging Asia revalues the CNY"

But the market is now in FX peg hunting mode and it appears that the only qualification needed to be a potential peg break goldmine is the word 'peg'. Some of the pegs appear to be being attacked by angry lynch mobs rather than reasoned investors. Take the Saudi real for example. It encapsulates the fears of whats happening next door in Yemen, Iraq and Syria, it captures the falling oil price and it encapsulates 'Emerging market' ( as much because most people have never heard of its currency rather than it actually being an emerging country). Ambrose Evans Pritchard* catapulting it to the fore a week or so ago also helped. But Saudi hardly have any debt and have about $670bio of reserves which would see them through 4 yrs of 20% budget deficits even if they never borrowed.

But why worry about the detail when you can just scream 'this is 1997' and ignore the background reserve structures. Even the Hong Kong Peg was being raised as a suitable peg break candidate today. Just do the reverse. If the Central banks had any sense they would be writing all the USD call options being bought against their currencies. Oh but they can't. No, but their Sovereign Wealth Funds may be able to. Even if they can't trade their own currency, they could come to an agreement and sell each others currency usd calls?

The Fed - Fed fed fed fed fed up with the amount of time wasted by humanity trying to guess what the Fed will do when actually the Fed are spending their time watching what you are doing to work out what they will do. I am still sticking with my March 2016 call which took 30 seconds to come up with two years ago and is still as valid then as it was now. Call it my $5 plastic cheapo Fed watch to everyone else's Patek Philippe Grande Taille Fed Chronograph. It still tells the same time and yet I have enough change to buy a boat and a car.

With the air thick with towels and me bleeding to death, I am wondering if I should also chuck my towel or just use it to staunch my blood loss. I am a stubborn fellow who really should know better but this is still august and I have to keep reminding myself that it is silly season. The market does suffer ADHD and though China, Emerging Markets, commodities and High Yield may look like the four horsemen of the apocalypse right now, only a month ago those Horsemen where Greece and Europe and they have effectively been turned into donkey rides. If attention can switch that rapidly before then it can happen again.

As I finish this post the markets have gone strangely quiet. Is that it? Are we done? Can we now get back to buying again? I hope so.

And one last thing . To the market acronyms of RORO and MOMO I would like to add one for the UK weather. SOSO - Summer On Sumer Off. This year has seen high frequency oscillations between Summer weather and November weather. Today is another November day.

---------------

*Has someone hacked Ambrose Evan Pritchard ? He wrote this about Chona and rather than calling for the end of the world he suggests quite the opposite in that China will be just fine. Odd. Also odd that John Ficenec has taken over the uber-apocalyptic role. Perhaps AEP has seen the light, is repenting his sins and becoming a missionary.